AUSTRALIA’S once strong grassfed bullock focussed production system has experienced rapid change in the past decade.

Ripley Atkinson

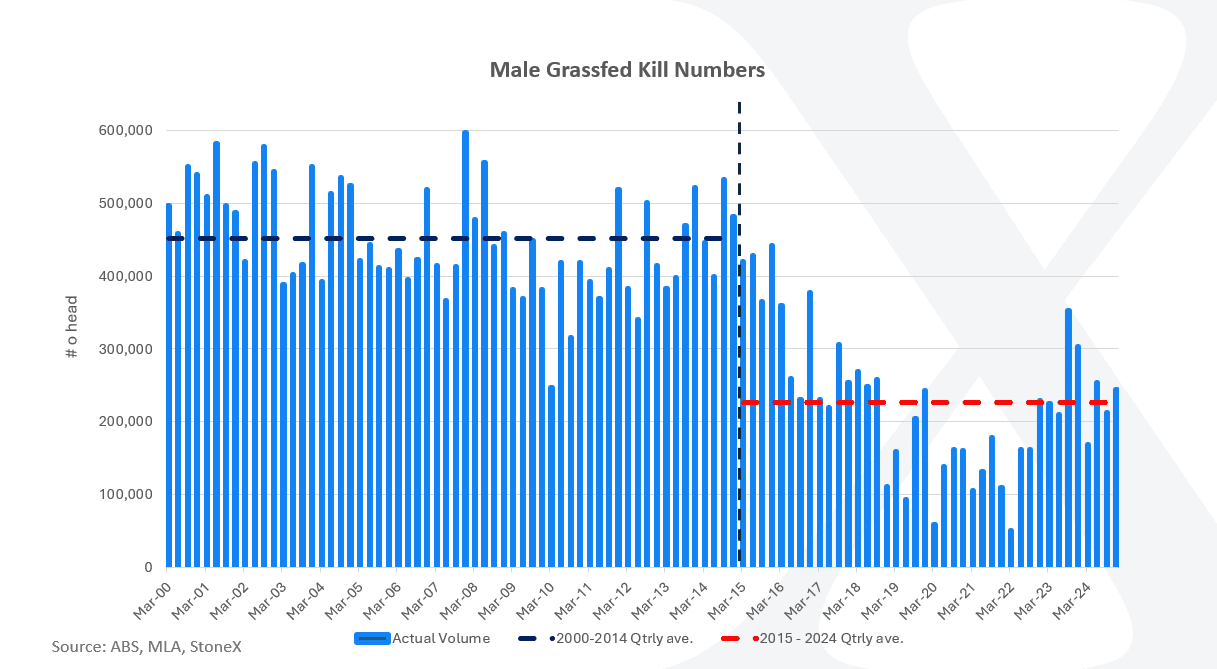

So significant, that quarterly grassfed male cattle slaughter has fallen by 50pc or 223,000 head on average from the 2000-2014 quarterly average, compared to the 2015-2024 quarterly average. Ultimately, the grassfed bullock production model never truly recovered following the herd liquidation years of 2013-15, as producers pivoted to have a clear focus on becoming a feeder centric production system.

In Figure 1, grassfed male kill numbers on a quarterly basis are represented as a bar chart, on the left hand axis, the two dotted lines in black and red running horizontal, represent the quarterly average grassfed male kill volumes between 2000-14 and 2015-24. Showing the stark decline in grassfed male kill numbers between the two periods.

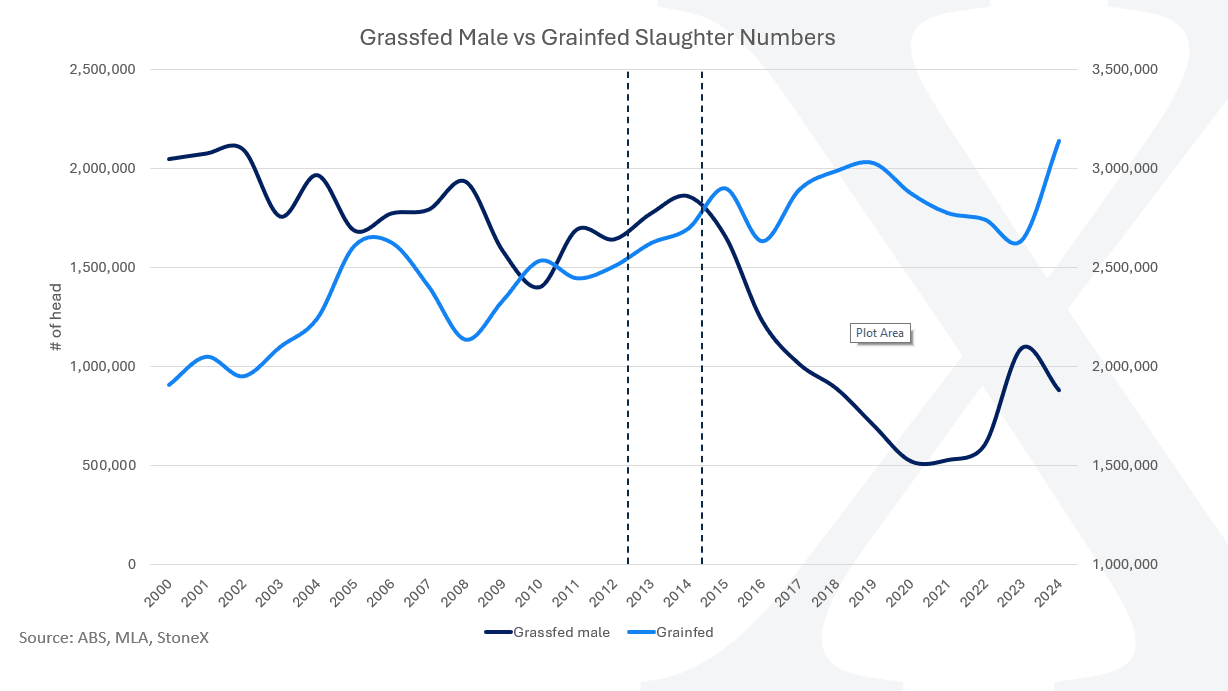

Figure 2 below provides further evidence to the shift Australian producers have made to their marketing channels since 2015. The chart examines yearly grassfed male kill numbers versus grainfed slaughter. The two dotted vertical lines represent the 2013-15 drought period, where the transformation to a feeder steer centric production model began.

Admittedly, due to current reporting structures, there is no way to decipher fed cattle slaughter into sexes, it is reported as a combination of male and female fed cattle, which means heifers are included in the grainfed slaughter volumes.

The trend is clear though, grassfed bullock production in Australia since 2015 has experienced sharp supply reductions in the face of the grainfed system in Australia growing substantially.

Drivers of the change to a feeder centric model

There are several reasons for this transformation;

- The ability to carry more breeding cows with feeder progeny are turned off at a younger age, reducing pressure on grass budgets – as heavier grassfed steers consume more than a lighter feeder.

- Significant variability in seasonal conditions limiting the ability of producers to carry steers through to bullock weights.

- The lot feeding sector diversifying its feeding programs to suit different cattle types, from shortfed supermarket and 100-day cattle through to longer fed Wagyu programs.

- Signals from the market for more consistent delivery of beef supply both from a seasonal and quality aspect (this is not to discount the high quality grassfed product we produce).

Further evidence to this shift is major beef export processing facilities across the country investing in their kill chains to handle heavier carcase weights delivered by grainfed cattle. Examples include JBS Dinmore, AMG Cootamundra, ACC Cannon Hill and TFI Murray Bridge, with these businesses adjusting processing floor plans, upgrading cold storage capacity in the chillers for larger carcases and improving boning room capacity, all to do with handling heavier grainfed cattle.

I have previously stated on this episode of the StoneX Australian Cattle & Beef Market Report podcast that I believed the 2017-19 drought was the turning point for the restructuring of the beef industries cattle marketing strategies when in fact it was clearly the 2013-15 drought.

What does this mean?

When analysing these figures and applying industry knowledge alongside the data, we can begin to paint a picture of how certain events can change the sector.

For readers, this information provides unique insights into how the beef industry has changed over the longer term and subsequently communicates information of importance to the bigger drivers and factors that influence the beef industry.

Understanding larger macro-economic trends ensures you remain informed and ahead of the pack in terms of industry information.

This analysis may assist producers with more strategic decision making such as transition away from or into grassfed bullock production.

Source: StoneEX

- For more on this topic, read Beef Central’s previous article on Queensland bullocks becoming dinosaurs.

HAVE YOUR SAY